What you need to know

about saving for retirement

Higher pension

By accumulating funds in all three tiers of the pension system, your income in old age can reach 70–80% of your pre-retirement income. Currently, the Sodra pension amounts to slightly more than 40% of your previous income. The longer you invest, the more you can expect to accumulate.

Tax incentives

On 1 January 2025, an amendment adopted by the Seimas came into force, according to which the personal income tax (PIT) relief no longer applies from 1 January 2025. For contracts that were concluded and took effect before 31 December 2024, the PIT relief will remain in force for a further 10 years, i.e., until 1 January 2035.

Flexibility and inheritance

You decide which funds to invest in, how much to contribute, how often to pay, and when and how to receive payments. The funds accumulated in the third-pillar pension fund are inheritable. You will be able to choose the method of payment that you find most attractive.

Take care of your future – save for retirement independently

Become a customer anywhere – from home, the office, or while traveling.

Our benefits

Largest volume of assets under management

We are the largest pension fund manager in terms of assets in Lithuania, managing more than 40% of the country’s total pension fund assets in the third pillar.

Experience

Over 30 years of investment and asset management experience. Your pension funds are given special attention.

It’s easy

You can become a client either by visiting any of our customer service units or via the self-service portal.

How to start saving

in the third pillar?

Choose a pension fund

We recommend that you choose a fund based on your age or risk tolerance. Keep in mind that your relatives or employer may also contribute, so make sure you arrange this in advance.

Conclude a pension contract

You can conclude a third pillar pension contract either by visiting any of our bank’s customer service units or via the pension self-service portal with Smart-ID or Mobile-ID mobile signature.

Set up regular payments

You can make contributions to your pension fund account on a periodic basis, for example monthly, and over a long period of time, which helps you to manage investment risk. It is advisable to save 10-15% of your income.

Choose a third pillar pension fund

based on your age

To achieve an optimal risk-return ratio, it is recommended that you choose a third pillar pension fund based on your age. Younger people are advised to choose funds that invest more in equities, while older people are advised to choose funds with a higher proportion of bonds and a lower proportion of equities.

So, once you reach a certain age, you should switch to a less risky fund. Check which pension fund is appropriate for your age to ensure that your retirement savings and investments are managed as efficiently as possible.

Up to 47 years of age

The recommended proportion of investment in equities is up to 100%.

From 47 to 58 years of age

The recommended proportion of investment in equities

is up to 70%, with the remainder invested in bonds or other conservative asset classes.

From 58 to 65 years of age

The recommended proportion of investment in bonds or other conservative asset classes is 100%.

Comparison of Artea Ambitious funds

You can sign up for one, two, or all three fund accumulation agreements. Below are the main features to help you choose.

|

|

Ambitious 16+ |

Ambitious Index 16+ |

Ambitious Active 16+ |

|

|

Which one is best for you? |

This is the best choice if you want to accumulate funds in the most popularpension fund among our clients. The fund is managed by combining active and index tracking (passive) management. Suitable for long-term accumulation. |

The most suitable for you if you want an index tracking (passive) strategy. The fund promotes sustainability (ESG) features. The fund has the lowest management fee. |

Best for you if you believe in active fund management. Suitable for those who want to start saving with smaller amounts or invest for a shorter period (up to 10 years). |

|

|

Sustainability |

At least 50% of investments are aligned with environmental and social (ESG) characteristics (compliant with Article 8 of the SFDR). |

At least 80% are aligned with environmental and social (ESG) characteristics (compliant with Article 8 of the SFDR). |

At least 50% of investments are aligned with environmental and social (ESG) characteristics (compliant with Article 8 of the SFDR). |

|

|

Geographical distribution of investments |

Largest investments |

North America, Western Europe, Asia and Oceania, Baltic States. |

North America, Western Europe, Asia and Oceania, Baltic States. |

North America, Western and Central Europe, Western Europe, Baltic States. |

|

Are investments made in China? |

No. |

Yes, because the fund is managed according to an index tracking strategy, and the tracked index includes China. |

No. |

|

|

Fluctuations in fund performance |

Historically, the fluctuations in this fund's performance since its inception have been lower than those of the benchmark index. Source: Bank of Lithuania (https://www.lb.lt/lt/pf-veiklos-rodikliai). |

The fluctuations in this fund's performance may be greater and depend entirely on changes in the benchmark index. |

Historically, this fund's performance fluctuations have been the lowest, but it should be noted that active management entails other risks arising from greater geographical allocation in Central Europe. |

|

|

Equity share |

Up to 100 % |

Up to 100 % |

Up to 100 % |

|

|

Management fee |

0,8 % |

0,59 % |

1,5 % |

|

|

Initial fee ** |

30% (min. EUR 100, max. EUR 200, during the first 12 months). Not applicable – when transferring pension fund assets exceeding EUR 2,000. |

30% (min 200 EUR, max 300 EUR, during the first 12 months). Not applicable – when transferring pension fund assets exceeding EUR 2,000. |

Not applicable. |

|

|

Target share of actively managed investments by fund managers |

Approximately 30 % |

0 % |

>50 % |

|

|

Strategy features |

Passive strategy |

Active strategy |

||

** A discount may be applied to employer contributions. All fees and their application are disclosed in the pension fund rules rules.

Third pillar pension fund results

Review the returns of third pillar pension funds and compare the results of different funds.

Saving for retirement

with the employer

Did you know that your employer can become a partner investing in your future?

accumulate more in the third pillar

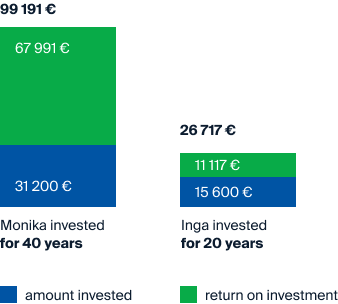

The longer you invest, the more you are likely to earn. This is due to the compound interest effect, where interest is earned on the amount deposited in the fund, as well as on the interest earned. In other words, your assets in the fund consist of contributions, interest earned and growth on interest earned. Of course, markets can go up and down, but in the long run, market fluctuations tend to even out. This is likely to result in a higher return on investment.

For example, the client Inga earned EUR 0.71 for every EUR 1 invested over a 20-year investment period. Monika has been investing for 40 years, and every euro she invested earned her EUR 2.18. This example confirms the compound interest effect described above in the long term.

How long should I save for retirement?

The amount you save will depend on when you start investing.

Important to know

Investing involves investment risk. The value of investments can go up or down. You may get back less than you invested. Past investment performance does not guarantee the same results and returns in the future. The calculations were performed using the MoneySmart calculator and are based on theoretical models under the conditions specified in the models and are illustrative, but are not a reliable indicator of future performance. The calculations are based on the following conditions: a monthly investment of EUR 65 and an average annual return of 5% after applicable taxes.

Although you can pay towards the third pillar pension at your convenience, regular contributions will help you build up your funds faster and help you grow the overall value of your assets in your third pillar pension fund. The most convenient way is to use an e-invoice service. With this tool, you can set your desired contribution rate and the preferred date for transferring funds to your third pillar account, e.g., upon receipt of your salary. This way you can be sure that you don’t forget to make regular transfers.

To attract and retain loyal employees, companies are increasingly focusing on ways to incentivise staff in the long term. One of these is additional saving for the employee’s future well-being. It is important to note that employees can also initiate their own pension savings at their employer’s expense. Visit your nearest customer service unit of Artea Bank and we will provide you with more detailed information and explain more about the possibilities related to employer-initiated supplementary retirement savings.

Log in to the pension self-service portal to access your notifications and see the details of your third pillar pension contract. Check whether your contributions are sufficient to build up the pension you want. When evaluating your accumulated assets, keep in mind that if markets have fluctuated and the fund’s returns have become negative for a while, it is likely that long-term savings will ultimately reduce the impact of the fluctuations on investment returns. We are ready to answer your questions, just make an enquiry and we will get back to you.

Third pillar pension benefits:

which payment options are available?

One-off benefit

You can withdraw all the funds you have accumulated in third pillar at once as a lump sum.

Periodic payments

You will receive regular payments from the pension fund and the remaining funds will continue to be invested.

Annuity

Payments within the remaining lifetime. This would require a contract with a life insurance company.

No income tax

You can withdraw the accumulated funds from the third pillar pension fund without additional tax when you have less than 5 years left until retirement and have been accumulating in the third pillar fund for more than 5 years.

Sign a contract

now!

Sign a contract

Sign a third-pillar pension accumulation contract online.

Fill out the inquiry form

Fill out the form and we will contact you.

Let's talk

Free customer service line, open Monday to Sunday from 8:00 a.m. to 8:00 p.m.

You may also be

interested in

Deposits

Artea offers some of the highest interest rates among the banks in the country.

Bonds

We have issued the largest number of bond issues in Lithuania.

Investment funds

Managers in our team are professionals, including some of the best investment managers in the world (according to Citywire).

Advanced securities trading platform

Invest into shares in the Baltic States and worldwide.

Second pillar pension

Pension accumulation in funds, allowing you to accumulate up to 20-30% of your former earnings for your pension.

When you participate in 3rd pillar pension funds, you will have to pay the fees set out in the rules of the pension fund you choose. The funds accumulated in the pension fund are invested in accordance with the investment strategy set out in the pension fund rules. When you save in pension funds, you take on the investment and investment-related risks. The value of a unit in a pension fund can go up or down, and you may get back less than you invested. A pension fund’s past performance does not guarantee the same results and returns in the future. Past performance is not a reliable indicator of future performance.

Before making an investment decision, you should assess all the risks involved in the investment yourself or with the help of an investment adviser, and familiarise yourself with the pension fund rules, which form an integral part of the supplementary voluntary pension agreement.

Pension benefits may be paid at the choice of the participant in the fund in the following ways: in one lump sum (lump-sum pension benefit), in regular instalments (periodic pension benefit), by converting the fund units in your Pension Account into cash and paying them out in regular instalments, or by purchasing an annuity from a life insurance company providing life assurance.

All the information contained herein is of a promotional nature and cannot be interpreted as a recommendation, offer or invitation to accumulate funds in pension funds managed by Artea Asset Management, the asset management company of Artea Bank Group. The information provided cannot form the basis of any subsequent transaction. Although the content of this promotional information is based on sources believed to be reliable, Artea Asset Management assumes no liability for any inaccuracies or changes in this information or for any losses that may arise as a result of investing based on this information.