Artea Pension 1982-1988 Index Plus

period

Main data

| Start of activities |

Managed by Artea Asset Management |

|||

| Latest data | Date |

Unit value |

Net assets |

|

| Change in value | Day's |

Month's |

3 months' |

Year's |

Investment strategy

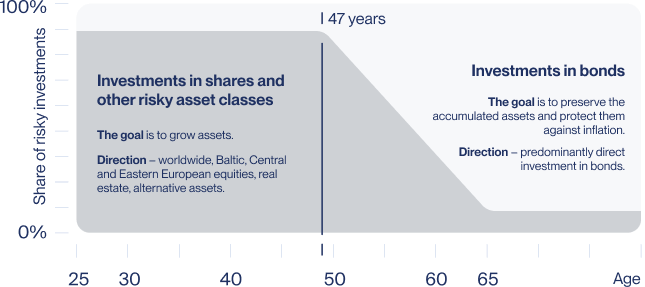

Artea Pension 1982-1988 Index Plus is a life-cycle fund for the target group of pension scheme participants within the set range of year of birth that invests in equities until its participants reach the age of 47. At 18 years before retirement, the fund starts to reduce the share of equities and increase the share of bonds. When the participant reaches the age of 64, the target is to have equities accounting for 10 percent in the fund, but this proportion can vary from 0 to 20 percent.

The benchmark index describes the fund’s investment strategy and is made up of indices representing individual asset classes. The fund’s performance against the benchmark index is measured by the tracking error, which is capped at 10 %.

The benchmark index varies over time based on the average age of the participant. The total share of risky asset classes decreases by 5.12%/n every working day (n – working days in the current year). The share of risky asset classes (i.e., equities) in the benchmark index of the Artea Pension 1982-1988 Index Plus fund will be reduced from the beginning of 2032 to a fixed share in 2049. At the same time, the share of less risky asset classes (i.e., money market instruments and bonds) is being increased.

Bond risk exposure is to be reduced in 2033 and additionally in 2039 and early 2045 by selecting benchmarks with lower maturities for euro area governments and investment-grade companies.

For more detailed information on benchmark movements, please refer to the investment strategy under “Description of the strategic pension asset allocation”.

Read more about the benchmark or its constituent indices here.

Composition as at 30 November 2023:

- 85% MSCI World IMI Net Total Return USD Index (converted to EUR) (M1WOIM Index)

- 12% MSCI Emerging Markets ex China Net Total Return USD Index (converted to EUR) (M1CXBRV Index)

- 3% European Central Bank ESTR OIS Index (OISESTR Index)

Composition as at 22 March 2022:

- 89% MSCI ACWI IMI Net Total Return USD Index (MIMUAWON Index) (converted to EUR)

- 8% MSCI Emerging Markets Net Total Return USD Index (M1EF Index) (converted to EUR)

- 3% European Central Bank ESTR OIS Index (OISESTR Index)

Composition as at 1 March 2021:

- 89% MSCI ACWI IMI Net Total Return USD Index (MIMUAWON Index) (converted to EUR)

- 8% MSCI Emerging Markets Net Total Return USD Index (M1EF Index) (converted to EUR)

- 3% European Central Bank ESTR OIS Index (OISESTR Index)

Composition as at 2 January 2019:

- 89% MSCI ACWI IMI Net Total Return USD Index (MIMUAWON Index) (converted to EUR)

- 8% MSCI Emerging Markets Net Total Return USD Index (M1EF Index) (converted to EUR)

- 3% EONIA Total Return Index (DBDCONIA Index)

Details of the depositary holding the pension fund’s assets:

SEB Bankas AB,

Konstitucijos pr. 24, 08105, Vilnius.

Sign the contract

now!

Sign the agreement

Sign a second pillar pension accumulation agreement online.

Fill out the form

Fill out the form and we will contact you.

Let’s talk

A free customer service line is available daily from 8:00 AM to 8:00 PM.

You may also be

interested in

Deposits

Artea offers some of the highest interest rates among the banks in the country.

Bonds

We have issued the largest number of bond issues in Lithuania.

Investment funds

Managers in our team are professionals, including some of the best investment managers in the world (according to Citywire).

Advanced securities trading platform

Invest into shares in the Baltic States and worldwide.

Important to know: we would like to remind you that for those participating in second-tier pension accumulation, the state social insurance old-age pension for the period until December 31, 2018, is proportionally reduced in accordance with the procedure established by law, except in cases where participants in pension accumulation until December 31, 2018, exercised their right to terminate their pension accumulation between January 1, 2019, and June 30, 2019, in which case the reduction of the state social insurance old-age pension will not apply to them. The amount of the old-age pension is not reduced due to the additional state contribution. A second-tier pension accumulation agreement cannot be terminated, except for the first second-tier pension accumulation agreement, which the participant has the right to terminate unilaterally within 30 calendar days of the conclusion of the agreement, upon loss of 70-100% of participation, upon diagnosis of a serious illness according to the approved list or upon determination of the need for palliative care services, or 5 years or less before retirement, if up to half of the mandatory annuity amount has been accumulated, upon notification of the pension accumulation company. Persons who became participants before December 31, 2018, had the right to terminate their participation in pension accumulation or suspend the transfer of pension contributions to the pension fund from January 1, 2019, to June 30, 2019.

Investing in pension funds involves investment risk. The pension accumulation company does not guarantee the profitability of pension funds. The value of a pension fund unit may rise or fall. You may get back less than you invested. Past performance of a pension fund does not guarantee the same results and profitability in the future. Past performance is not a reliable indicator of future results.

We recommend that you choose your pension fund responsibly and carefully, pay attention to the risks associated with investments, the applicable deductions, and carefully read the pension fund rules, which are an integral part of the pension accumulation agreement.

Depending on the amount accumulated in the second-tier pension fund, it will be possible to withdraw it as a lump sum or in periodic payments (when up to €16,785 has been accumulated) or to purchase a pension annuity (when between €16,785 and €83,926 has been accumulated), which can be of three types: standard, inheritable standard, or deferred. If a standard annuity is chosen, the entire accumulated amount is allocated to the purchase of the annuity, and annuity payments begin immediately and are paid for the rest of the participant's life. If you choose a inheritable standard annuity, the annuity payments are also paid for the rest of your life, and at the same time, payments are guaranteed until the participant reaches the age of 85 – this means that if the participant does not reach this age, the amount not paid out until the age of 85 is inheritable. In both cases, the entire amount accumulated in the pension fund is used to purchase the annuity, and the annuity payments are paid by Sodra. If you choose a deferred annuity, the pension accumulation company pays periodic payments until the age of 85 (a portion of the assets is allocated for this purpose, after deducting the funds for the purchase of the deferred annuity), and these funds will be inherited, while from the age of 85, Sodra pays the annuity payments for the rest of the participant's life. If more than €83,926 has been accumulated, the portion of the assets exceeding this amount may be paid out as a one-time pension payment, and the remaining portion is paid according to the type of annuity purchased. You can find out more about pension annuities here.

All information provided is of an advertising nature and cannot be interpreted as a recommendation, offer or invitation to accumulate funds in pension funds managed by Artea Asset Management, the asset management company of the Artea Bank group. The information provided cannot be used as a basis for any subsequent transaction. Although the content of this promotional information is based on sources that are considered reliable, Artea Bank and Artea Asset Management are not responsible for any inaccuracies or changes in this information, nor for any losses that may arise when investments are based on this information.